Jefferies Warns Stablecoins Could Drain Up to 5% of Bank Deposits by 2030

Jefferies analysts project stablecoin market cap could reach $1.15 trillion within five years, gradually eroding traditional bank deposits and squeezing margins.

Digital Dollars Encroach on Banking Territory

Investment bank Jefferies has issued a stark warning about the growing competitive threat stablecoins pose to traditional banking. According to the firm's analysts, the stablecoin sector's market capitalization could reach $1.15 trillion within the next five years, triggering a gradual but significant migration of funds away from bank deposits.

The analysts emphasized that while digital dollars are unlikely to cause a sudden bank run, over a five-year horizon banks could lose between 3% and 5% of their core deposits. This erosion would inevitably raise funding costs and compress profit margins across the industry.

Why This Matters

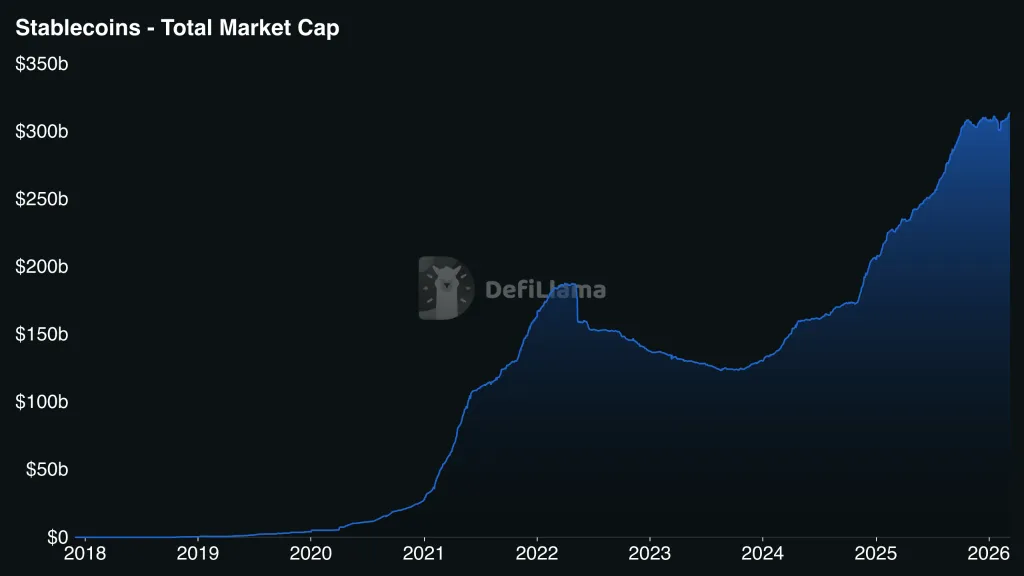

Stablecoins have evolved far beyond their origins as crypto trading tools. Following the passage of the Genius Act in the United States, their use cases expanded dramatically to include everyday payments, treasury management, and cross-border transfers. In 2025, adjusted stablecoin transfer volume exceeded $11.6 trillion — a 49% increase year-over-year.

The fundamental challenge for banks is that stablecoins operate as digital cash around the clock and provide access to DeFi platforms offering yields that outpace traditional savings accounts. Bank of America CEO Brian Moynihan has previously warned that the U.S. banking system could lose up to $6 trillion in deposits. The Bank Policy Institute expressed similar concerns, citing U.S. Treasury Department research.

Regulation: The Key Restraint

Jefferies highlighted the market structure bill known as the Clarity Act as a potential counterbalance. In its current form, the legislation limits the appeal of stablecoins as savings instruments by designating them strictly as payment tools. According to Jefferies, the Clarity Act would close the "yield loophole" left open by the Genius Act. However, whether the bill passes in this exact form remains uncertain.

Banks Race to Adapt

Some major financial institutions are already responding. Fidelity Investments has launched its own stablecoin, FIDD. Bank of America and Goldman Sachs are exploring similar initiatives to issue their own digital dollar tokens.

Nevertheless, Jefferies identified banks with heavy exposure to retail and interest-bearing deposits as facing the greatest risk. The firm's analysts specifically flagged Wintrust, Flagstar, WBS, EagleBank, and Axos as the most vulnerable institutions. By contrast, large institutional players and custodians already investing in crypto infrastructure are significantly better positioned to weather the shift.

Jefferies' projection of stablecoin market cap reaching $800 billion to $1.15 trillion by 2030 underscores the systemic nature of this transformation. Pressure on traditional bank funding will intensify in proportion to the expanding role of digital dollars in the real economy.

Frequently Asked Questions

How much could banks lose in deposits due to stablecoins?

Jefferies estimates banks could lose 3% to 5% of their core deposits over a five-year period. Bank of America CEO Brian Moynihan has warned the U.S. system could shed up to $6 trillion in deposits overall.

What is the stablecoin market cap forecast for 2030?

Jefferies projects stablecoin market capitalization will grow to between $800 billion and $1.15 trillion by 2030. The sector's current total market cap stands at approximately $314 billion.

Which banks are most at risk from stablecoin growth?

Jefferies identified Wintrust, Flagstar, WBS, EagleBank, and Axos as the most vulnerable institutions. Banks with high exposure to retail and interest-bearing deposits face the greatest risk of deposit erosion.

What is the Clarity Act and how does it affect stablecoins?

The Clarity Act is a U.S. market structure bill that would designate stablecoins strictly as payment instruments rather than savings tools. According to Jefferies, it would close the 'yield loophole' left by the Genius Act, though its final passage remains uncertain.

Are traditional banks launching their own stablecoins?

Yes. Fidelity Investments has already launched a stablecoin called FIDD. Bank of America and Goldman Sachs are exploring similar initiatives to compete in the digital dollar space.

Read also

Stablecoin Transfer Volume Hits $10.5 Trillion in January — Highest Since April 2022

January stablecoin transaction volume surpassed $10.5 trillion, marking the highest monthly figure since April 2022. USDC led transfers while USDT maintained market cap dominance.

Top 10 Dollar Stablecoins in 2026: From Dominant Players to Exit Candidates

The stablecoin market has surpassed $311 billion in total capitalization. Here's a breakdown of the ten largest USD-pegged stablecoins — from undisputed leaders Tether and Circle to ambitious newcomers.

Weekly Recap: Bitcoin Tests $74K, Miners Dump Holdings, ChatGPT Boycott Grows

Bitcoin briefly touched $74,000 before retreating to $67,500. Public miners sold over 15,000 BTC in five months, traders flocked to Hyperliquid for oil and gold futures, and a ChatGPT boycott gained major traction.

TON Wallet Introduces Yield Vaults for BTC, ETH, and USDT Directly in Telegram

TON Wallet has launched yield vaults for BTC, ETH, and USDT directly within Telegram, offering up to 18% APY on stablecoins through partnerships with Morpho, TAC, and Re7.

Weekly Recap: Aave Ecosystem Rescue Mobilizes 100,000 ETH and Quantum Computer Cracks 15-Bit ECC Key

Bitcoin held near $78,000, the DeFi community rallied over 100,000 ETH to help Aave recover from the Kelp hack, and a researcher cracked a 15-bit ECC key on a quantum computer.

TRON Energy Rental: How to Cut USDT Transfer Fees by Up to 60%

USDT issuance on TRON surpassed $85 billion in February 2026, but transfer fees remain steep at $1.83–$3.83 per transaction. Energy rental services like TronZap offer a way to cut costs by 50–60%.